Transfer Pricing Without Group Valuation: A Smarter Approach

When Transfer Prices Distort the True Cost Picture

In multi-entity manufacturing groups, goods rarely stay within a single legal entity. Raw materials are produced in one country, transformed in another, and sold from a third. At each handover, an intercompany transfer price is charged; often including a markup above the actual production cost. This is standard practice for tax compliance and arm's-length pricing regulations. But it creates a problem that haunts finance teams at period-end: the cost that lands in inventory at the receiving plant is not the same as the true economic cost to the group.

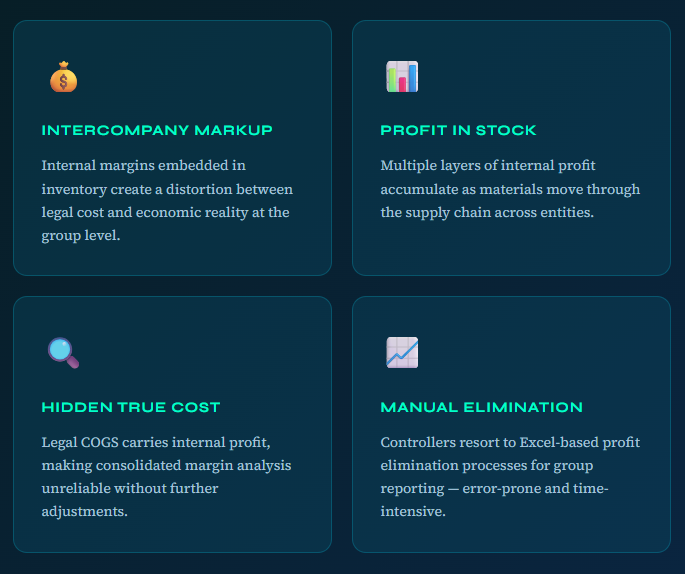

That embedded markup is not a real expense; it is internal profit simply moving from one pocket to another within the same consolidated group. Yet in most SAP implementations, this markup is silently baked into inventory values and COGS, inflating legal cost, distorting margin analysis, and forcing controllers into time-consuming manual Excel-based eliminations just to understand what consolidated profitability actually looks like.

For years, SAP's answer to this challenge was the Group Valuation currency type; a parallel ledger within the Material Ledger designed to hold a separate cost view stripped of intercompany margins. In theory, it solves the problem elegantly. In practice, it introduces significant implementation complexity, data governance overhead, and constraints that many organizations find disproportionate to the benefit. There is, however, a smarter path, one that achieves the same analytical outcome without activating Group Valuation at all.

This article explores that approach: Parallel Actual Costing via the Alternative Valuation Run (AVR) in SAP S/4HANA. We will walk through the business problem, the mechanics of the solution, its five-layer architecture, and the concrete benefits it delivers for finance and controlling teams.

Understanding the Problem: Profit Hidden Inside Inventory

The Four Core Business Problems

These four problems compound each other. An intercompany markup might be just $20 on a single material in a single period, but across thousands of materials, dozens of plants, and multiple supply chain tiers, the cumulative embedded profit in inventory can be material. When this inventory is sold, the inflated COGS understates the group's true gross margin. When it sits in stock, the balance sheet overstates inventory value from a group consolidation standpoint.

The conventional SAP remedy, activating the Group Valuation currency type, requires system changes at Material Ledger configuration level that are extremely difficult to reverse, and it introduces a parallel set of postings that must be reconciled continuously. For organizations already running on S/4HANA with Actual Costing active, there is a far less invasive solution available.

The Cost Flow Challenge: A Worked Example

To make this concrete, consider a simple two-plant scenario. Plant A manufactures Raw Material X at an actual cost of $100. It sells this material to Plant B under an intercompany arrangement, charging a $20 transfer price markup for a total of $120. Plant B then applies a further $50 of transformation cost — labour, machine time, overhead absorption — to produce Semi-Finished Product Y.

Intercompany Supply Chain Cost Accumulation

From a legal accounting perspective, Plant B's inventory correctly carries $170; the transfer price it actually paid plus its own transformation cost. This is the figure that flows into its statutory accounts, satisfying local GAAP requirements and supporting the arm's-length pricing documentation. From a group perspective, however, the true economic cost of Semi-Finished Y is only $150: the original $100 of raw material cost plus $50 of real transformation work. The $20 markup is a fiction at the group level; it cancels out in consolidation.

This $20 gap is precisely what Parallel Actual Costing is designed to surface, quantify, and eliminate — automatically, at material level, using SAP's own cost engine — without touching the legal valuation or requiring Group Valuation currency type activation.

The Solution: Five Layers of Architecture

The Parallel Actual Costing framework for group valuation is built on five sequential layers, each with a distinct function. Together, they create a complete dual-view costing system that runs alongside the standard Material Ledger actual costing process without interfering with legal valuation.

Legal Actual Costing Layer

Official Material Ledger actual costing for statutory accounting and legal valuation. No changes are made here, legal values remain fully intact for local GAAP and tax purposes.

Group Valuation Rule Layer

Business rules define exactly which cost components constitute intercompany markup. Transformation costs are preserved. Internal freight margins are isolated and classified separately.

Parallel AVR Layer

The Alternative Valuation Run calculates group actual cost using the actual quantity structure but applies different valuation rules, stripping out the intercompany markup from each cost component.

Extension Layer

BAdI-based custom logic identifies intercompany procurement sources, splits markup by supply chain tier, and reclassifies values for precise cost component attribution across plants and company codes.

Analytical Reporting Layer

CDS views, SAC dashboards, and Fiori applications expose the legal vs. group cost bridge by material, plant, profit center, and company code, enabling real-time consolidated margin analysis.

Analytical Reporting Layer

CDS views, SAC dashboards, and Fiori applications expose the legal vs. group cost bridge by material, plant, profit centre, and company code, enabling real-time consolidated margin analysis.

Layers 1 and 2 are the technical foundation. The key insight is that the Alternative Valuation Run is not a separate costing run in the traditional sense; it reuses the actual quantity structure that the standard actual costing run has already determined. This means the physical flows (how much of each input was consumed, where it came from, at what quantity) are identical between the legal and group views. The only difference is the price applied to intercompany-sourced components.

Layer 3 is where the business intelligence lives. Defining which components represent genuine intercompany markup, as distinct from legitimate service charges, freight costs, or currency adjustments, requires careful analysis of the organization's transfer pricing policies. Done well, this layer ensures that the group cost view reflects economic reality rather than an arbitrary exclusion of all intercompany postings.

Layer 4 provides the flexibility to handle real-world complexity. Multi-tier supply chains, where Material X from Plant A is incorporated into a sub-assembly at Plant B before being used by Plant C, require markup stacking logic. The BAdI framework enables custom code to trace markup through multiple levels of the BOM structure, ensuring that cumulative internal profit is correctly identified at every tier.

Layer 5 closes the loop by making the dual valuation data consumable. Without reporting, the most technically elegant costing solution delivers no value. CDS views bridge the Material Ledger cost component data into the analytical layer, while SAC and Fiori apps surface the legal-versus-group bridge in a format that business users, not just SAP specialists, can act on.

Business Benefits: What This Unlocks for Your Organization

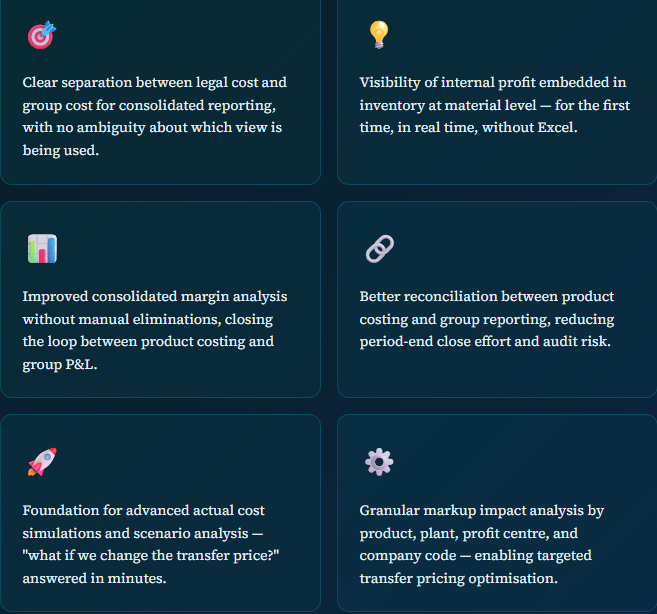

The benefits of this approach extend well beyond cleaner numbers. They fundamentally change what finance and controlling teams can see, analyse, and decide.

Perhaps the most transformative benefit is the last one. When markup impact can be analyzed by product and plant, transfer pricing conversations shift from a compliance exercise to a strategic tool. Business units can see precisely how their sourcing decisions affect group margin, and pricing teams can model the consolidated impact of proposed rate changes before they are implemented.

There is also a significant audit and governance benefit. Manual Excel eliminations introduce reconciliation risk; figures can differ depending on who ran the spreadsheet, when it was last updated, or which version of the transfer price list was used. By embedding the elimination logic inside SAP's actual costing engine, controlled through formal configuration and BAdI exits, the group cost view becomes an auditable, repeatable, system-generated output.

Conclusion: Transform Your Cost Visibility Without the Complexity

Transfer pricing has always sat at the intersection of tax compliance and management accounting, and that intersection has historically been an uncomfortable place for ERP systems to operate. The instinct to solve it at the configuration level, by activating Group Valuation currency types is understandable, but it often trades one set of problems for another.

The Parallel Actual Costing approach using the Alternative Valuation Run represents a more surgical solution. It preserves everything that legal valuation needs to preserve — statutory compliance, tax documentation, local GAAP — while creating a parallel, system-generated group cost view that eliminates intercompany markup at material level across the entire supply chain.

The result is a dual-view costing architecture that enables finance teams to answer the questions that matter most to the business: What is our true consolidated cost of goods sold? How much internal profit is embedded in our inventory? Where in the supply chain is transfer pricing creating the largest distortion, and what is the quantified impact?

For SAP S/4HANA organizations running Material Ledger Actual Costing, this capability is already within reach. The framework is not a bespoke build, it leverages standard SAP functionality (the AVR) extended with targeted BAdI logic and surfaced through the existing analytical stack of CDS views and SAC. The implementation challenge is primarily one of design and configuration, not infrastructure.

At ERPfixers, we specialize in exactly this kind of precision SAP consulting; solving complex costing and finance challenges that standard documentation alone cannot answer. If your organization is struggling with transfer price distortion in inventory, manual elimination processes at period-end, or a gap between your legal COGS and your economic margin, we would welcome the conversation.

Contact ERPfixers today and, be sure to subscribe to our YouTube channel, where we share valuable webcasts and video series on a range of SAP topics.

📺Subscribe to our YouTube Channel

📧Send us an email Info@ERPfixers.com

📱Call us at +1 (302) 551-3627

📅Set an appointment today CALENDAR